A practical guide to using UM/UIM coverage when the other driver has no insurance—or not enough

UM vs. UIM in plain English

Idaho insurers must provide UM/UIM disclosures and typically offer these coverages alongside your policy, with limits that often match your bodily injury liability limits unless you choose otherwise. In many situations, you can reject UM/UIM in writing—but that decision can become painfully expensive after a serious crash.

Why this matters in Boise and the Treasure Valley

For construction managers, contractors, and business owners, the consequences of an uninsured-driver crash can be amplified: missed site time, project delays, and physical work restrictions can quickly turn into real financial pressure. UM/UIM coverage is designed to reduce that risk—but only if the claim is handled correctly.

Did you know? Quick UM/UIM facts Idaho drivers miss

What a UM/UIM claim can help pay for

| Category | Examples | What helps prove it |

|---|---|---|

| Medical costs | ER, imaging, PT, follow-up care, meds | Itemized bills, treatment notes, referral plan |

| Lost income | Missed shifts, reduced duty, lost contracts | Pay stubs, job logs, contract records, doctor restrictions |

| Pain & disruption | Reduced mobility, sleep issues, headaches | Consistent treatment, symptom journaling, witness notes |

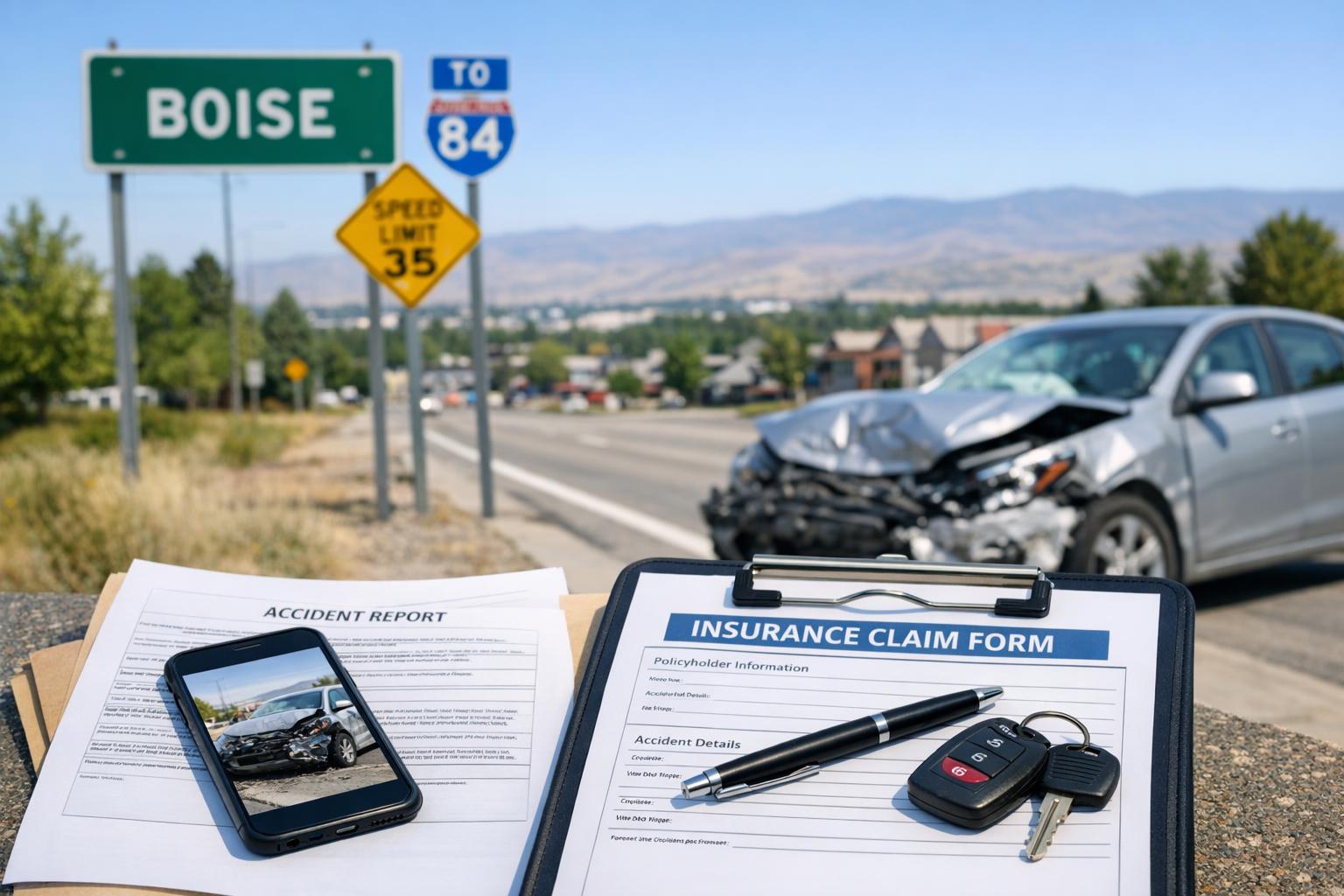

Step-by-step: What to do after an uninsured-driver accident in Idaho

1) Call law enforcement and document the scene

2) Get medical care quickly—and follow through

3) Notify your insurer—but be careful with recorded statements

4) Pull your declarations page and look for UM/UIM limits

5) Track losses like a business (because insurers do)

6) Watch deadlines—Idaho injury claims are not open-ended

When UM/UIM claims get complicated (and what that can look like)

Local angle: Boise-area considerations that affect UM/UIM claims

2) Multi-vehicle impacts: Chain-reaction crashes can create disputes about who is “legally responsible” and how UM/UIM applies.

3) County-level crash trends: Idaho’s crash reporting includes county and city breakdowns showing how local crash patterns can shift year-to-year—useful context when thinking about risk and coverage choices in Ada County and the Boise area.